The 86,420 Hidden Traps: Why a Collateral Registry Search is Mandatory Before Buying Property in Ghana

Imagine finding the perfect plot of land in a prime area of Accra. Better yet, the seller is offering it to you at a price five times cheaper than the average market rate for that neighborhood.

When you ask why the price is so unbelievably low, the owner looks you in the eye and gives a perfectly relatable reason: “I am relocating abroad next week, and I need to liquidate my assets immediately. I just need a fast cash sale.”

It feels like a once-in-a-lifetime goldmine. Afraid of losing out to another buyer, you rush through the basic paperwork, hand over your hard-earned money, and celebrate your incredible luck.

Months later, you clear the land and prepare to lay your foundation, only to be stopped by representatives from a commercial bank accompanied by security personnel.

As they hand you court-ordered foreclosure documents, the devastating reality sets in: the previous owner didn’t give you a “good deal.” They used that exact land as collateral to secure a massive bank loan, defaulted, and fled the country. You didn’t buy property at a discount; you just bought someone else’s massive debt at a premium price.

In Ghana’s competitive real estate market, this nightmare plays out all too often. Fortunately, it is entirely preventable if you know how to look past surface-level ownership.

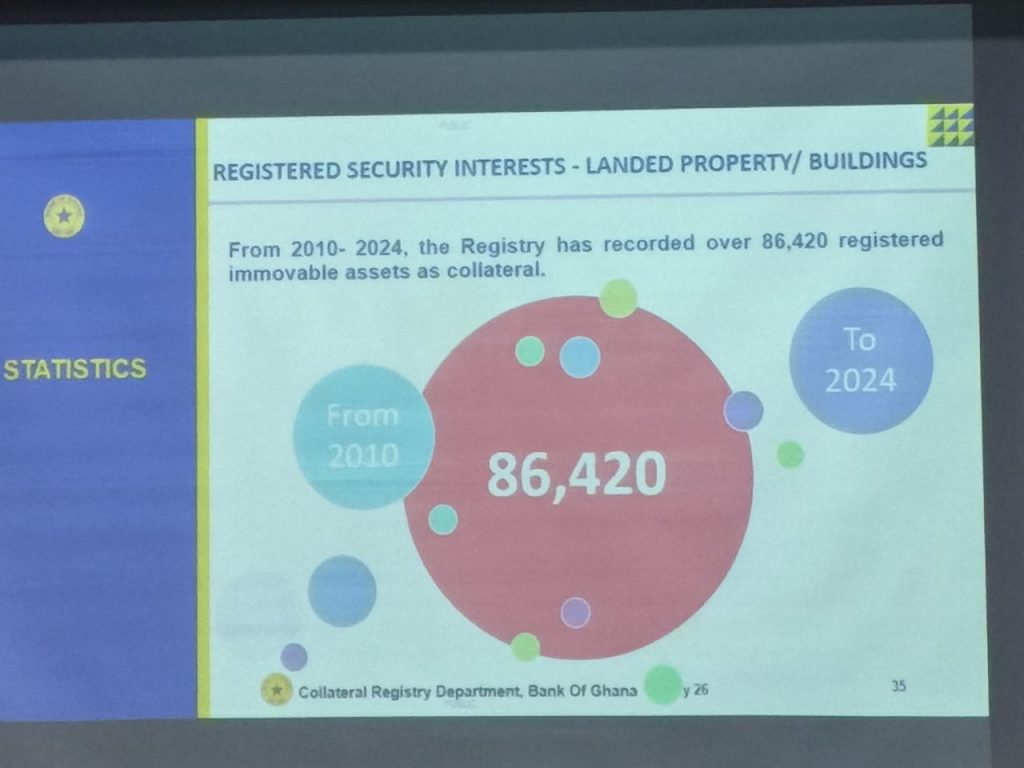

The Reality Check: Over 86,420 Properties Pledged as Collateral

A live statistic released by the Collateral Registry Department of the Bank of Ghana sheds light on the massive scale of property currently being used as financial leverage across the country.

According to official records, between 2010 and 2024, the Registry recorded over 86,420 registered immovable assets (landed properties and buildings) as collateral.

What does this mean for a prospective property buyer? It means there are nearly 90,000 properties across Ghana that, while they may look completely ready for a clean sale, are legally tied to active bank loans, credit lines, or corporate debts.

READ ALSO: Nungua vs. Tse Addo: Which Coastal Neighborhood is Your Perfect Match?

If you unknowingly buy a property that has an active “security interest” registered against it, you inherit that liability. Under the Borrowers and Lenders Act, 2020 (Act 1052), financial institutions retain the legal right to seize and auction the property to recover their money if the original borrower defaults—regardless of whether ownership was transferred to you.

Putting the Numbers in Perspective: How Big is the Risk?

To truly grasp the importance of a Collateral Registry search in Ghana, it helps to look at how this figure compares to the overall pool of structures in the country.

According to the Ghana Statistical Service (GSS) Population and Housing Census, there are roughly 10.6 million total structures across Ghana (with about 8.5 million being fully completed).

At first glance, 86,420 registered collaterals might seem like a small fraction of the entire nation’s housing stock.

However, the risk intensifies dramatically when you factor in market realities. Here is a breakdown of the numbers based on the information we have:

| Property Category | Approximate Metric | The Risk Factor |

| Total Nationwide Structures | ~10.6 Million | Includes rural dwellings, informal kiosks, and un-serviced family lands that banks will never accept for a formal loan. |

| Active Urban Real Estate Market | Highly Concentrated | Banks overwhelmingly accept collateral located in prime urban centers (e.g., Accra, Tema, Kumasi, Takoradi). |

| The Danger Zone | Estimated 1 in every 15–20 high-value urban properties | In prime, formalized areas where you are actually looking to buy a home or land, a significant portion of active properties carry hidden bank encumbrances. |

Because commercial banks and tier-1 lenders rarely accept informal or rural properties as loan security, the 86,420+ registered collaterals highlighted are heavily concentrated in the exact urban real estate markets where you are looking to invest.

Why a Standard Lands Commission Search is No Longer Enough

Many property buyers believe that a routine title search at the Lands Commission is a bulletproof guarantee of a clean sale. This is a dangerous misconception.

While the Lands Commission verifies legal ownership and title history, it does not always capture real-time financial encumbrances created by commercial banks, microfinance institutions, or rural banks.

The Bank of Ghana’s Collateral Registry was specifically designed to bridge this information gap, functioning as a master ledger for assets pledged to secure financial facilities.

A thorough vetting process must include:

- Lands Commission Search: To verify who legally owns the land.

- Collateral Registry Search: To verify if that owner has pawned the land to a financial institution.

Protect Your Investment: Work With a Verified Real Estate Agent

Navigating the intersection of property law and banking regulations in Ghana can be complex. Missing a single detail, failing to track down family stool land dynamics, or using the wrong search criteria (such as a slight misspelling of a borrower’s corporate name) can yield a false clear result, leaving your capital dangerously exposed.

This is why working with an experienced, professional real estate agent is vital. A professional agent does not just “find houses”—they manage your risk.

They will collaborate with legal experts to conduct comprehensive due diligence, checking both the Lands Commission and the Bank of Ghana Collateral Registry before you part with a single cedi.

Furthermore, an agent understands true market valuations, ensuring you don’t fall prey to “too good to be true” pricing traps while negotiating the best possible deal on a genuinely clean asset.

Are you ready to purchase property safely?

Click here to contact a verified real estate agent to initiate a comprehensive Collateral Registry and title search today, ensuring your future home is 100% yours.